INVESTMENT : at RETIREMENT

- LIFE ANNUITY(with guarantees)

Your decision on a Life Annuity is final and irrevocable.

A life annuity protects you against the risk of outliving your capital.

You choose the following :

- A guaranteed period (between 0 and 25 years.

(A longer period reduces your monthly income)

- Annual increase percentagebetween 0 and 6%.

(A higher increase reduces your initial monthly income)

- Reduce your monthly incometo 80% or lesser, activated by the death of the partner who passes away first. This reduction only starts at the end of the guaranteed period.

(A higher reduction increases your initial monthly income)

- These choices influence your monthly income

A. Single Life Annuity

You receive a fixed / guaranteedmonthly income (fully taxable) as long as you live. Should you die before the guaranteed period expires, the fullannuity is paid to your appointed beneficiary/ies up to the end of the guaranteed period and then stops. Your beneficiary has the option between an annuity or the remaining cash. Should you outlive the guaranteed period, the full annuity is paid till you die and then stops. Your capital is not preserved upon your death.

B. Joint and Survivorship Annuity(Partner and Life partner)

You receive a fixedmonthly income (fully taxable) up to death of the surviving partner. Should you and your partner die before the guaranteed periodexpires, the full annuity is paid to your appointed beneficiary/ies up to the end of the guaranteed period and then stops. Your beneficiary has the option between an annuity or the remaining cash. Should you and/or your partner outlive the guaranteed period, the annuity is paid up to the death of the surviving partner and then stops. Upon death of an partner, the income reduces to your chosen percentage (if applicable), only after the guaranteed period expired. Your capital is not preserved upon your and / or your partner’s death.

2. LIVING ANNIUTY(no guarantees)

Your decision on a Living Annuity is not final. If needed you may exercise the option changing to a Life

Annuity. However, you decision on a Life Annuity then become final and irrevocable.

- You can manage your investment portfolio

- Your income/capital is not guaranteed.

- Your income is fully taxable.

- Your level of income may be higher or lower than other conventional annuity options.

- Switching between funds at any stage, but charged for.

- Transparency of investment composition and performance.

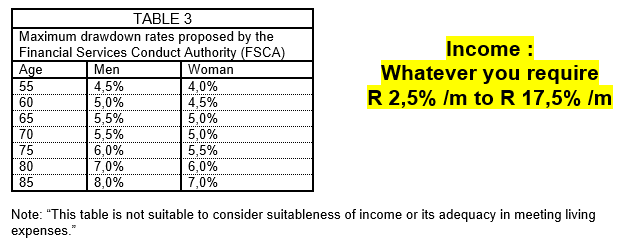

- You may select the rate (and reselect the rate on anniversary) of your annual income as 2,5% to 17,5% of the market value of your investment. This rate depends on your income needs (monthly budget). Your choice may be limited to the growth of investment (positive or negative).

A small selected drawdown rate may lead to capital growth.

A high selected drawdown rate may lead to capital liquidation.

- You are exposed to the following risks :

- living too long (longelivety)

- poor market conditions

- excessive upfront and / or ongoing fees and charges

- high drawdown rate to meet your income needs (monthly budget) Refer to Table 3 which could result in

the following poor retirement outcomes :

- poor investment returns on your retirement capital

- your retirement capital becomes depleted before you die

- an unsustainable income stream

- a reduction in income payments

- poor health to perform future decisions on income

- On each investment anniversary the income amount for the next year is calculated as: “selected income percentage times current market value of the fund.”

- Capital preservation at death without life assurance.

Upon your death, your beneficiary has the choice to carry on receiving the monthly income or to have

the capital (with growth) to be paid out.

- You may convert to a conventional life annuity with guarantees at a later stage.