- MEDICAL AID

When you apply and become a member of an open medical scheme :

– You agree to abide by the rules for membership and declare that all information

provided by you is true, correct and complete. You have to provide information on yourself, your spouse / partner and your dependants about any medical condition, symptom or illness even if you do not consider it relevant to your application. If not, the medical scheme may cancel any membership and / or refuse to pay your medical expenses.

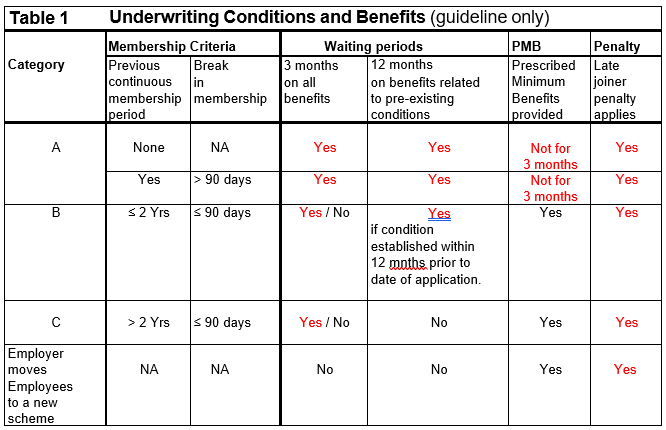

– The medical scheme may apply waiting periods during which time it does not pay

for any or certain expenses immediately after you become a member. However, you have to pay the normal monthly contributions during these waiting periods. This prevents you from joining a medical scheme only when you are sick and need benefits. Refer to Table 1

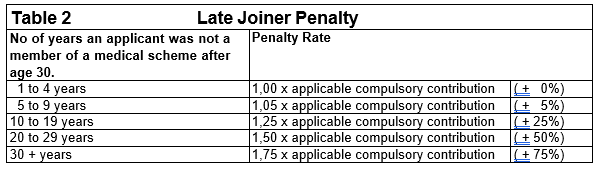

– The medical scheme may impose late joiner penalty feeswhich penalty is permanentand transferred to other medical schemes. A late joiner is a person 35 years and older. This penalty dependants on the number of years that a late joiner did not have medical scheme cover. Refer to Table 2

– You have to provide proof of all registered South African medical schemes that you previously belonged to in

the form of a membership certificate.

– You have to pay your contributions on time every month to avoid suspension of benefits.

– You may have money available in advance on your medical savings account to use for day-to-day medical expenses (glasses, dentistry, doctor visits, medicine etc) during the financial year. If you resign from the scheme, you may owe the scheme money or the scheme may owe you money. The funds you do not use during a financial year rolls over to the next year.

– The scheme has the right to amend (add, delete, change) benefits and to amend monthly contributions from time to time. This normally happens at the end of their financial year.

– Income verification will be conducted by the medical scheme if you choose benefits provided for the lower income band. Income is normally considered as the higher of the main member’s or spouse’s / partner’s gross earnings.

– You are covered for 270 conditions on any plan (high and low premium plans) you select. This list of conditions is referred to as Prescribed Minimum Benefits. It ensures that all members have access to certain minimum benefits. Refer to Table 1

NOTES

– It is illegal to be a member of more than one medical scheme at the same time. If you belong to a medical

scheme, you need to end your membership before your join a new scheme.

– Medical schemes offer different plans at different premiums. If you choose a plan based mainly on affordability

you must realise that less expensive plans offer lesser benefits and more exclusions. For example, if you choose

a plan that covers hospitalisation only (“hospital plan” without “day-to-day” benefits) you might not have access to

the “trauma recovery extender” benefit. Trauma recovery includes but is not limited to after care rehabilitation

needed due to an accident or stroke. Rehabilitation might stretch over weeks or months and be unaffordable

without a trauma recovery benefit.

– Some benefits may require a co-payment from your own pocket.

– The scheme has the right to amendbenefits and contributions. This normally happens on an annual basis. It is

your responsibilityto familiarise yourself with your chosen plan’s latest benefit and contribution schedule.

– You have to contact the medical scheme and / or it’s providers upfront to obtain pre-authorisation for planned

medical procedures.

– It is in your interest to enquire from your medical scheme upfront the amount they allow for planned medical

procedures and whether your service provider charges you medical aid rates, because you are responsible for

the difference.

– You are allowed to upgradeyour plan at the end of the financial year only (normally November – December of

each year).